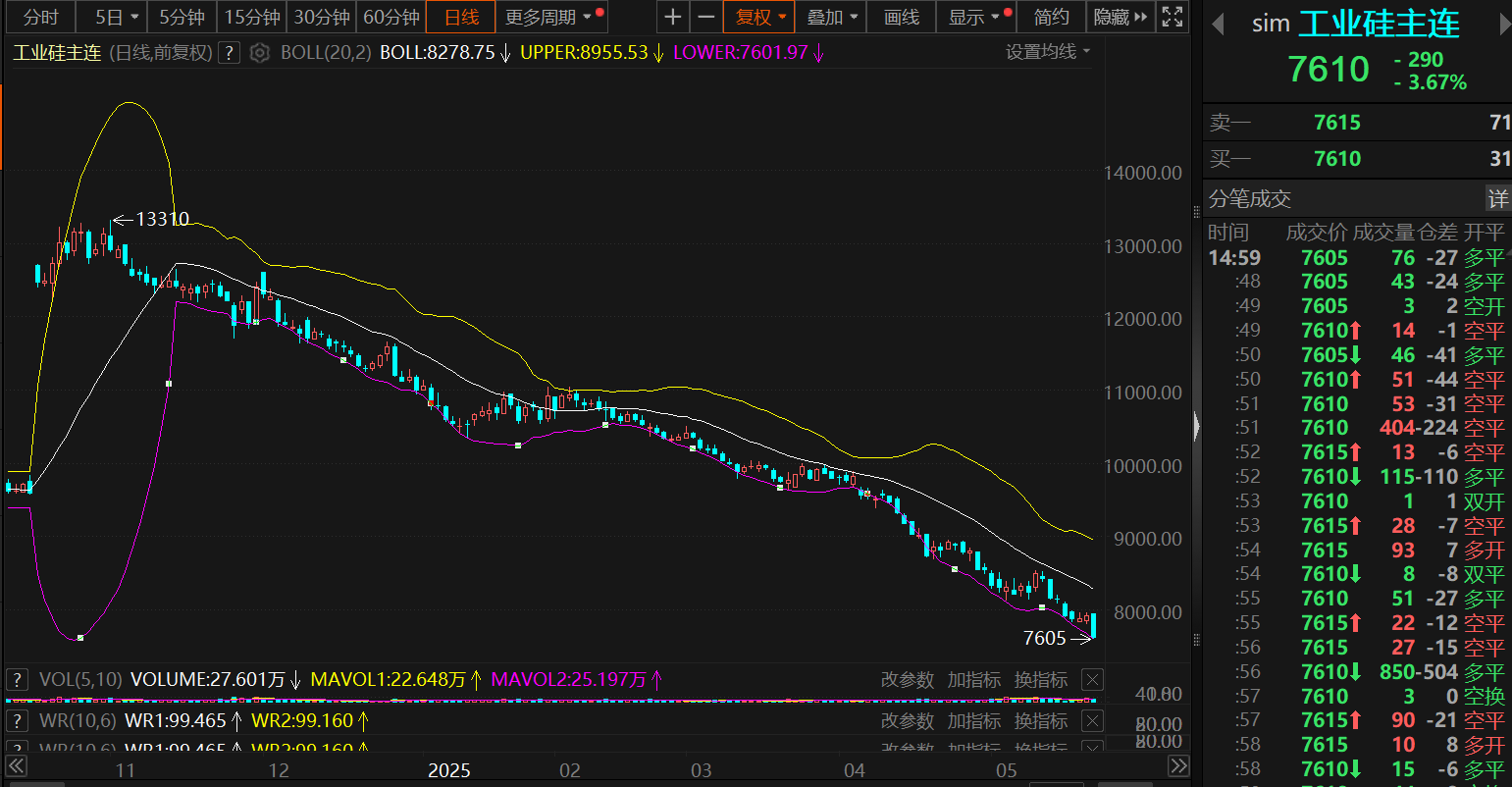

SMM News on May 26: On May 26, the main silicon metal futures contract continued to decline after the opening bell, hitting a record low of 7,605 yuan/mt during the session. By the end of the daytime trading session, the main contract closed at 7,610 yuan/mt, down 3.67%.

In terms of spot prices, silicon metal spot quotes also continued to fall. As of May 26,oxygen-blown #553 silicon (east China)spot quotes fell to the range of 8,500-8,700 yuan/mt, with an average price of 8,600 yuan/mt, also hitting a record low.

》Click to view SMM's spot quotes for silicon products

Regarding the reasons behind the continuous decline in silicon metal futures and spot prices, SMM believes it is mainly related to the weak fundamental performance of silicon metal oversupply.

According to SMM's supply-demand balance calculations, the surplus of silicon metal in Q1 was around 45,000 mt. From April to May, the market showed a situation of weak supply and demand, with the supply-demand balance shifting towards a slight destocking, but the magnitude was relatively small, having little impact on the supply-demand structure. In June, with the resumption of production and an increase in supply from some capacities on the supply side, the balance may once again shift towards inventory buildup.

Specifically, on the supply side, according to SMM's understanding, entering June, a major plant in Xinjiang is expected to resume production. Additionally, as Yunnan and Sichuan enter the rainy season, local silicon enterprises may also resume production one after another. Although it is expected that the operating rates of local enterprises may decrease compared to previous years, the resumption of production by enterprises will still generate a certain increase in supply. Therefore, SMM expects that supply will show an increasing trend in June, July, and August.

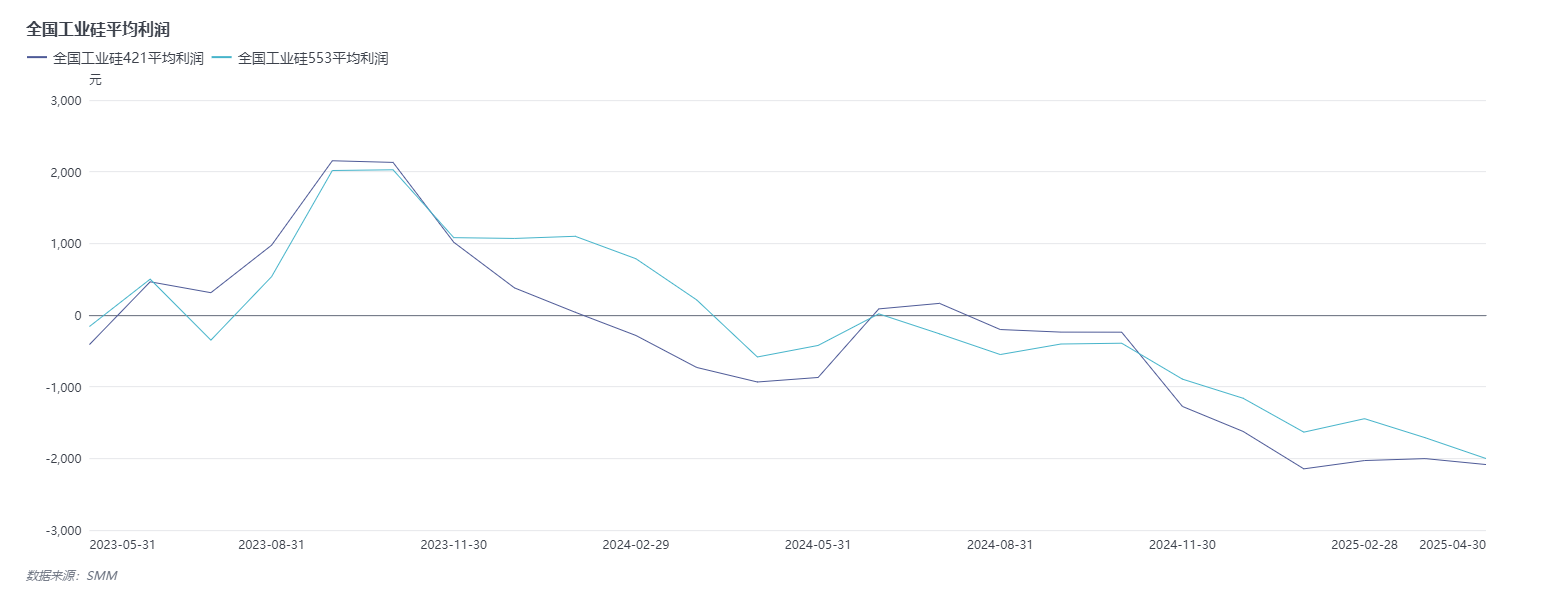

On the cost side, according to SMM's understanding, the prices of silicon coal and electrodes on the cost side have both decreased compared to the previous period. However, due to the simultaneous decline in silicon metal prices, the losses of silicon enterprises have not been alleviated. As of the end of April 2025, SMM's monthly operating rate for metal silicon fell to 51.23%, which is at a relatively low level in recent years.

In contrast to the increase in supply on the supply side, the performance on the demand side has been largely stable. According to SMM's survey last week, the operating rate of polysilicon remained basically stable, with individual silicon powder tender orders being released. Subsequent attention should be paid to the transaction situation of silicon powder. In terms of silicone, the operating rate increased slightly on a WoW basis last week, with some monomer enterprises completing maintenance of their facilities. The industry's operating rate is expected to rise to above 60%. For aluminum-silicon alloy enterprises, the operating rate remained stable last week, with silicon metal being purchased as needed. SMM expects that there will not be many outstanding expected performances on the demand side in the future, with a relatively stable performance and a not-so-large increase in demand.

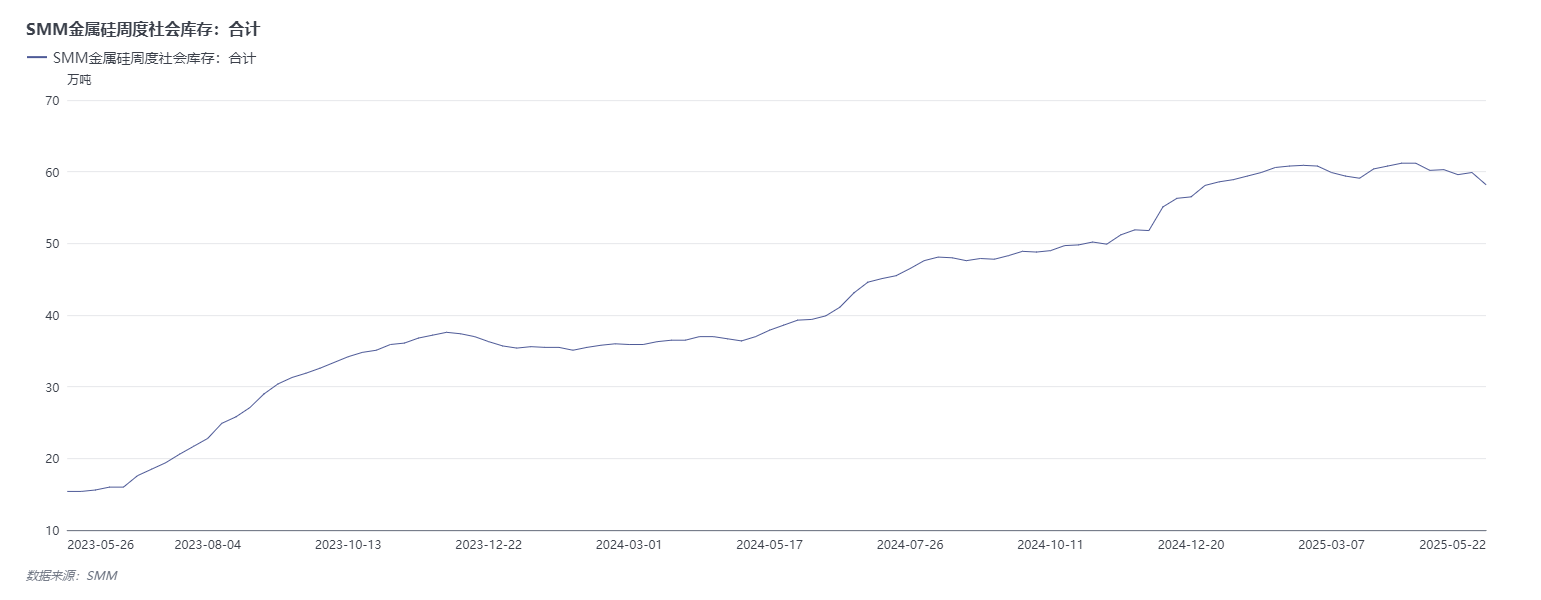

In terms of inventory, due to the sharp decline in silicon metal prices last week, with prices continuously hitting record lows, market transaction sentiment improved somewhat. Therefore, social inventory decreased last week. SMM's statistics show that the total social inventory of silicon metal in major regions was 582,000 mt on May 22, down 17,000 mt WoW. Among them, social general warehouses held 130,000 mt, a decrease of 2,000 mt WoW. Social delivery warehouses held 452,000 mt (including unregistered warrants and spot cargo), an increase of 15,000 mt WoW. However, considering that inventory levels remain near highs in recent years, the brief and relatively small destocking cannot provide significant support to silicon metal prices.

Overall, the current high inventory situation of silicon metal cannot be alleviated temporarily, and the imbalance between supply and demand still exists. The expected increase in supply over the next few months and the mediocre performance on the demand side will lead to a supply surplus in the silicon metal market. Therefore, SMM expects that the momentum for silicon metal prices to stop falling and rebound in the short term is slightly insufficient, and prices are expected to continue fluctuating at lows. Subsequently, attention should be paid to the possibility of production cuts by large plants on the supply side amid the backdrop of silicon metal prices continuing to hit new lows.

Institutional Comments

Zhongcai Futures stated that, from a fundamental perspective, large plants in Xinjiang may gradually resume production, the operating rate of silicon plants in north-west China remains stable, and some silicon plants in Yunnan have resumed production. Overall, the decline in supply pressure will gradually ease. On the demand side, polysilicon production in May declined slightly MoM. In June, with the resumption of production by some polysilicon plants, production may increase slightly. Some silicone enterprises have resumed production, and their operating rates have increased. The operating rates of secondary aluminum alloy enterprises continue to decline, constrained by insufficient orders and losses. Overall, south-west China is about to enter the rainy season, and some enterprises have resumed production slightly. Recently, the market has heard that large plants in Xinjiang plan to resume production in May and June. Currently, it is difficult for silicon metal demand to pick up. If the resumption of production by large plants materializes, the surplus pressure on silicon metal will further increase. In the short term, silicon metal is expected to maintain a doldrums trend, and attention should be paid to the strategy of shorting on rallies.

Industrial Futures stated that the weak trend in silicon metal futures is difficult to reverse, and the overall strategy remains bearish. In terms of silicon metal supply, the number of furnaces in operation has declined, and overall production has weakened slightly. Factories in south-west China have started and stopped operations, while the number of furnaces in operation in Xinjiang has increased. The pressure on the supply side of the market remains relatively large in May. On the demand side, polysilicon enterprises in south-west China have relatively weak willingness to resume production and are expected to start production in July. There may be equal or reduced substitution, which will have a relatively small boosting effect on silicon metal demand. The operating rates in the silicone industry have recovered slightly, with silicone plants in Shandong and Zhejiang completing maintenance and increasing production. Overall, in the short term, demand-driven growth is insufficient, and silicon prices remain under pressure. Subsequently, attention should be paid to the furnace operation situation in south-west China during the rainy season.

SDIC Futures stated that, on the supply side, according to SMM, large plants in Xinjiang plan to resume production in June, coupled with the resumption of production by silicon plants in the Sichuan production area, the expected supply volume will further increase. SMM's latest total social inventory stands at a high of 582,000 mt. Against the backdrop of weak main demand, there are signs of a recovery in operating rates across various silicon metal production areas. It is expected that prices will continue to fluctuate at lows in the short term, but the downward trend is difficult to reverse.

Xinhu Futures stated that polysilicon prices are under weak pressure and remain stable on a MoM basis. Some enterprises have reduced their operating rates and production, while downstream procurement remains relatively cautious, with ongoing negotiations between buyers and sellers. Silicone prices have stabilized, and the industry has plans to reduce operating rates and refuse to budge on prices. In the short term, the rush to export in downstream industries provides some support for demand, but the current supply and demand situation in the industry still appears loose. Aluminum alloy prices are running smoothly, with average sales performance. The operating rates of primary aluminum alloy production have declined somewhat, while those of secondary aluminum alloy production have remained stable. Industry inventory has decreased on a MoM basis, with a certain decline in warrant volumes, and factory inventories continue to shift to the market. With expectations of growth in industry supply, the risk of inventory buildup in the industry increases, putting continued pressure on silicon prices. In the short term, the futures market is expected to remain in the doldrums, and it is recommended to hold short positions and continue to pay attention to the calendar spread strategy.

Guangzhou Futures stated that, from a fundamental perspective, as the rainy season gradually approaches in the southwest region, enthusiasm for production resumptions has decreased compared to previous years, but there is still room for production resumptions. At the same time, the release of some new capacity and potential production resumption plans by large factories in the north are expected to increase supply. Given the persistent weakness in demand, inventory pressure remains significant, which may continue to suppress the rebound potential of the futures market. Strategically, the approach of selling on rallies should be maintained.